Pennsylvania allows a 90% Pa education improvement (EITC) tax credit for a two year contribution to a qualified organization where funds are used for Pa k-12 tuition scholarships, preschool scholarships, and education improvement. In 2014 Pa allowed special purpose entities (SPE’s) to accept investments and EITC tax credit awards as long as investors work for a business or own a business. The Pa EITC SPE program allows any qualified individual to redirect their Pa taxes to scholarships for families and children at the school of their choice. In 2010 the IRS advised a full donation deduction for contributions and reduced state tax payments for tax credit amounts in a chief counsel memorandum.

In 2018 a new federal tax law limited personal state and local itemized deductions to $10,000. Several states like New York and New Jersey with high state taxes passed laws to allow “charitable contributions “ in return for tax credits to public trusts that were used to fund government operations. The IRS issued Notice 2018-54 warning that they were going to issue regulations limiting these tax credit schemes used by high tax states.

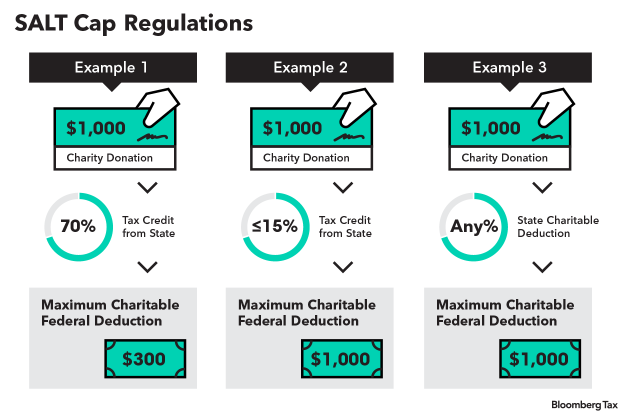

On August 24, 2018 the IRS issued temporary regulations with the concept of “quid pro quo” adjustments to any donation that included a state or local tax credit benefit in excess of 15% (below 15% is considered deminimis in the regulation). Since the donor received a tax credit benefit for the donation of a tax credit the donation needs reduced by the amount of the tax credit because of the quid pro quo nature of the donation. The IRS explained in light of the new $10,000 tax limitation, the minority of taxpayers involved and the fairness of tax policy they were issuing these regulations which changed the administration of taxes in this area of donations in which the taxpayer receives a tax credit. The 2010 memo was noted as being before the $10,000 individual state and local tax deduction limitation. The proposed regulation is effective August 28, 2018.

Example- In the past SPE federal tax form K-1 would have a $10,000 full donation deduction for an investment in the SPE of $10,000 and a SPE tax form PA K-1 tax credit of $9,000. After August 27, 2018 this same federal SPE K-1 form will reflect a $1000 donation deduction and a $9000 non deductible expense. The PA K-1 will still reflect a PA K-1 tax credit of $9000.

While independent PA EITC donors may consider donations on Monday to beat the regulation deadline it’s a risky strategy as tax credit award letters have not been issued yet. Our SPE will wait for tax credit award letters before accepting investments and remitting donations as has been past practice. Significant interest in our remaining PA EITC tax credits continues as this is still a wonderful efficient way to redirect your Pa taxes to local schools and children as scholarships at a minimal cost. Our SPEs expect to run out of credits in November so please submit joinders without donation checks to reserve your own Pa EITC tax credit.

The new regulation by the IRS impacted over 300 tax credit programs nationwide that had existed for many years so before year end there may be changes in the temporary regulations based on hearings in November on the new temporary regulations or there may be modifications in the federal “Tax 2.0” legislation for education tax credits expected to be passed before year end. The final treatment of K-1 reporting is still being studied for our charity and independent tax experts have been requested to assist so we are sure federal K-1s are accurate when sent out the first week of February 2019. No changes in the 90% Pa tax credit have been made by our charity or Pennsylvania.

We encourage each of our schools and donors to continue to participate in the Pennsylvania EITC program as it continues to assist education improvement in Pennsylvania for preschool, public school and private school children across the state and in your local schools.